| Written by Me Sébastien Fiset , LL.B., B.A.A. |

| Mardi, 16 Mars 2010 17:48 |

MAKE SURE YOU ARE FULLY COVERED !

Contact the author : s.fiset@fisetlegal.com

Some insurers make the mistake of regarding a condominium as a multi-unit immovable when an insurance quote for a syndicate is issued. Make no mistake.

And deciding on insurance may cost you more than you think! Be vigilant when it comes to choosing or renewing an insurance policy.

OUTLINE :

SYNDICATE :

The type if insurance required depends on the type of the co-ownership.

It is the primary responsibility of the syndicate to ensure the immovable in its entirety because this is linked to its main role: “the preservation of the immovable” (article 1039 of the Civil Code of Quebec).

Under article 1073 of the Civil Code of Quebec, the syndicate has an obligation to endorse insurance covering the whole immovable (from top to bottom, through the garden, parking, etc.), including the private fractions (apartments, interior), but excluding improvements made by a co-owner or his predecessors or even the “extra” that a developer would be granted at the sale.

We must be vigilant when choosing insurance. Some insurers, unaware of the meaning and purpose of article 1077 of the Civil Code of Quebec, refuse to cover the syndicate’s responsibility for damages caused to co-owners by faulty construction or design.

A syndicate must take an insurance against “ordinary risks” (fire, theft, vandalism, explosion, water damage, natural disasters, terrorist acts, hail, snow on the roof, etc.) AND third person liability insurance. The latter will cover the liability related to the “decisions taken by the board of directors” according to article 337 of the Civil Code of Quebec, as well as in the event of loss caused by buildings (a tile falling, slipping on the stairs, etc.). We must realise that if the “all risk” insurance of the syndicate does not provide sufficient coverage, the liability insurance of the syndicate will step in and costs will be higher ! It is therefore important to make sure that the protection against “ordinary risks” corresponds to the real value : the amount covered by the “all risk” insurance must correspond to the replacement value of the immovable and not otherwise. It is a legal obligation. Moreover, what would a syndicate do if it were unable to pay for the damages caused not only to the common areas of the immovable but also to the co-owners’ private fractions ?

The insurance policy covering the immovable must be issued in the name of the syndicate only, as it appears in the enterprise registrar.

To know the «replacement cost» of its immovable, a syndicate should request from a licensed appraiser, recognized by its association, a certificate of assessment of the immovable.

The syndicate may, once it has received the certificate of assessment, “shop” for an insurance that meets the immovable’s needs. It is very important to request an insurance policy that covers both the rehabilitation of the immovable, and the respect of the new requirements, new regulations on construction that may result in additional costs. Construction costs also increase with time; an up-date will be needed after a few years. Beware in case of defects or poor workmanship, the insurer has the right to refuse to cover the costs of such corrections.

It is also wise to choose an insurance that does not impose limits on benefits, for instance in case of backflow, and to always request the “replacement costs” in the insurance policy to ensure adequate comprensation.

CO-OWNER :

The syndicate’s insurance will not cover damage to a private fraction of a co-owner that affects the improvements that have been made by the co-owner himself or his predecessors. It does not cover the personal property (movables) of the co-owner or his liability or that of his tenants. It is therefore important for the owner of the private fraction to have an adequate insurance for the improvements and personal property as well as liability insurance.

A co-owner does not have to insure his share of the common parts because this would create an unnecessary multiplicity of insurance and could cause complications when claims are made.

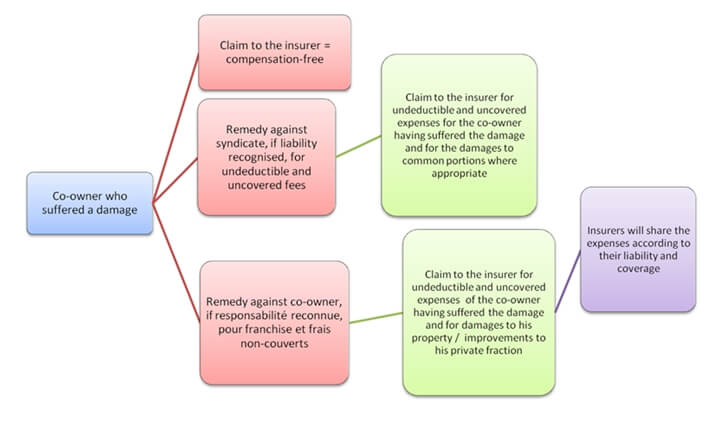

In case of loss…

Sometimes several insurers are involved for the same loss. Below is an illustration of how a claim should be directed in the event that damages affect the private fraction of a co-owner.

Whatever the nature of damage, both the syndicate and the co-owners are responsible to notify their insurer of any event that could be the object of a claim, however small this may be.

In case of plurality of insurances, it should generally be the syndicate’s at the forefront, especially when it comes to a substantial loss.

Important loss

Before 1994, declarations of co-ownership generally gave the syndicate the possibility to rebuild or not after substantial damage. An up-date of the declaration of co-ownership is necessary in order to respect article 1075 of the Civil Code of Quebec. It is the syndicate’s obligation to repair or rebuild unless the syndicate decides to terminate the co-ownership.

If the loss is «substantial», compensation should be paid to the trustee appointed in the constituting act or, failing that, appointed by the syndicate.

It is difficult to draw the line at determining which damage must be considered a «substantial loss». Some declarations of co-ownership address this issue, thus avoiding potential conflicts, specifying, for example, a percentage of the replacement value of the immovable or simply fixing an amount at which damage is considered major.

The trustee will be the syndicate’s most useful advisor in case of a major loss. He will supervise, in case of loss, the transfer of the indemnities and the reconstruction when there is a substantial loss in the immovable.

In the event of substantial loss, if the trustee decides to terminate the co-ownership, he will be responsible for managing the insurance and distributing, according to the share of the indemnity of each of the co-owners according to the relative value of his fraction, paying out of that share first the preferred and hypothecary creditors. However, certain conditions need to be met before such a decision is made.

Should the syndicate decide not to continue with the co-ownership, the indemnity will then be distributed to the hypothecary creditors that have priority, the balance will be submitted to the syndicate’s liquidator.

If the syndicate decides to continue with the co-ownership and it uses the services of a trustee, the latter will ensure that the indemnity is used only for reconstruction and repairs of the immovable, as it was originally.

It is therefore important to maintain a register containing the plans and specifications for the immovable : the insurer compensates the syndicate with the equivalent of the cost of replacement of the affected parts of the immovable as they were before the loss.

During the reconstruction after a major loss, sometimes the limits of the building change, which creates a need to redo the cadastral plan and the certificates of location of co-owners.

Before purchasing a co-ownership…

Any interested buyer should request from the vendor a copy of the assessment used to determine the replacement value of the immovable and a copy of the certificate of insurance of the immovable to determine if it is sufficiently covered.

For peace of mind…

Consult a professional in law specialising in co-ownership law. He will make things clear for you and advise you in case of doubt, in any situation.

The information provided on this page is general in nature and cannot compensate for the need to obtain legal advice specific to a particular situation.

Mise à jour le Samedi, 16 Août 2014 17:40